Although you can write a valid will yourself, it can be complicated if you have shared assets like houses or bank accounts or if you’ve been married or divorced. There are a number of ways you could write a will.

Firstly, a solicitor could produce a valid will for you. This may be the most expensive option in terms of upfront cost, but it could be the best value option if you have a number of people you’d like to inherit your estate, or if you think that inheritance tax may have to be paid. A good solicitor will help you plan your will around current inheritance tax laws, as well as giving you the peace of mind that the will would be valid and has been completed by a regulated professional.

You could use a will writing service available either by arranging a qualified will writer to visit your house or by doing it online. This is normally cheaper than using a solicitor. If you use a will writing professional, they should be a member of the ‘Institute of Professional Willwriters’ or ‘The Society of Will Writers’ which will mean that although they are not regulated in the same way as solicitors, they will have had to undertake training.

If you use an online company to do your will or use a shop bought pack, check the company’s reputation and reviews. There is no guarantee of the will being valid but this could be a good option if your plans are simple and do not require complex instructions.

Alternatively, many charities offer a solicitor will writing scheme at either a discounted cost in the form of a donation to the charity or for free. These wills are usually written or checked by a solicitor so you can have confidence in these wills.

There are also yearly events arranged by charities like ‘Free Wills Month’ and ‘Will Aid’. ‘Free Wills Month’ runs every March and October and allows anyone aged over 55 to get a will written by a solicitor for free. If you’re getting a will as a couple, only one of you needs to be over 55.

‘Will Aid’ runs every November and is available to people of any age. Solicitors involved waive their fee for writing or amending a basic will, and invite people to make a voluntary donation to ‘Will Aid’ which distributes funds to its partner charities.

Although these wills are advertised as free, it is hoped that you would make a donation to the charity or leave something to the charity in your will in exchange for the will writing service.

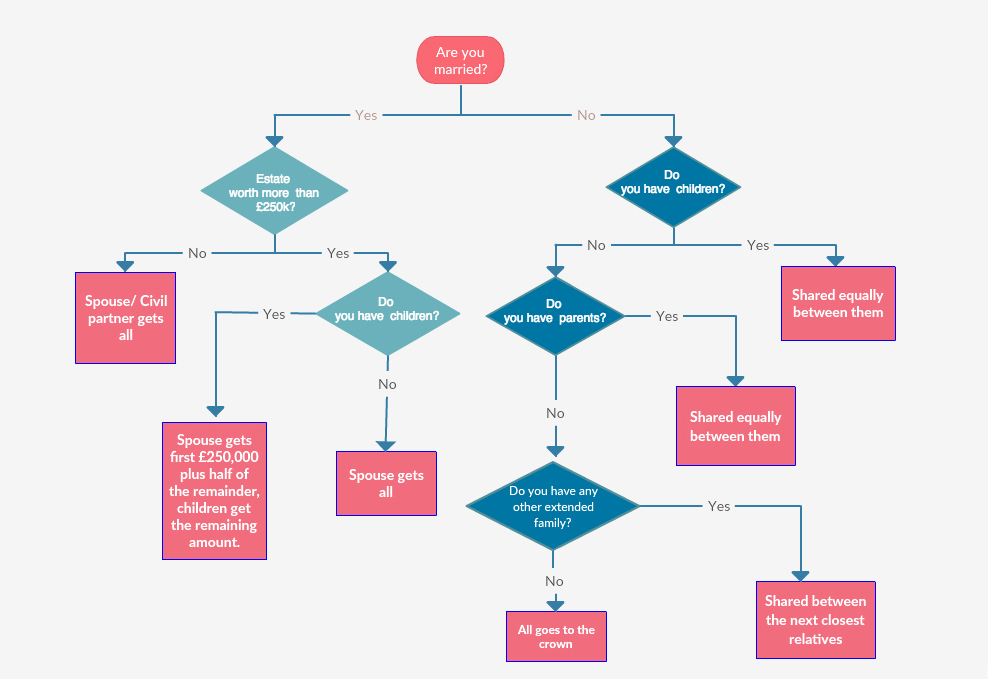

Once you’ve written a will it’s also important to update it after any major life events. A marriage or divorce will automatically revoke a will, meaning the estate is subject to intestacy laws covered in the intestacy section. Although this is useful as people are not likely to want to leave inheritance to a former partner, it can also be a bad thing as all the other directions in the will are invalid too.